Buying a new home is a massive financial decision in any market. In a super competitive one like we’re seeing today, waiting probably feels like the most responsible decision.

The National Association of Realtors has reported that homes are selling in 17 days or less. Bidding wars are being sparked between buyers with over 4.5 offers on the average home.

But today’s housing market is best described as a moving train. The longer you wait to get on, the harder it will be to catch up.

DEMAND WILL CONTINUE TO OUTPACE SUPPLY

The low number of homes for sale has dipped us into a seller’s market and supply has not been able to catch up with demand.

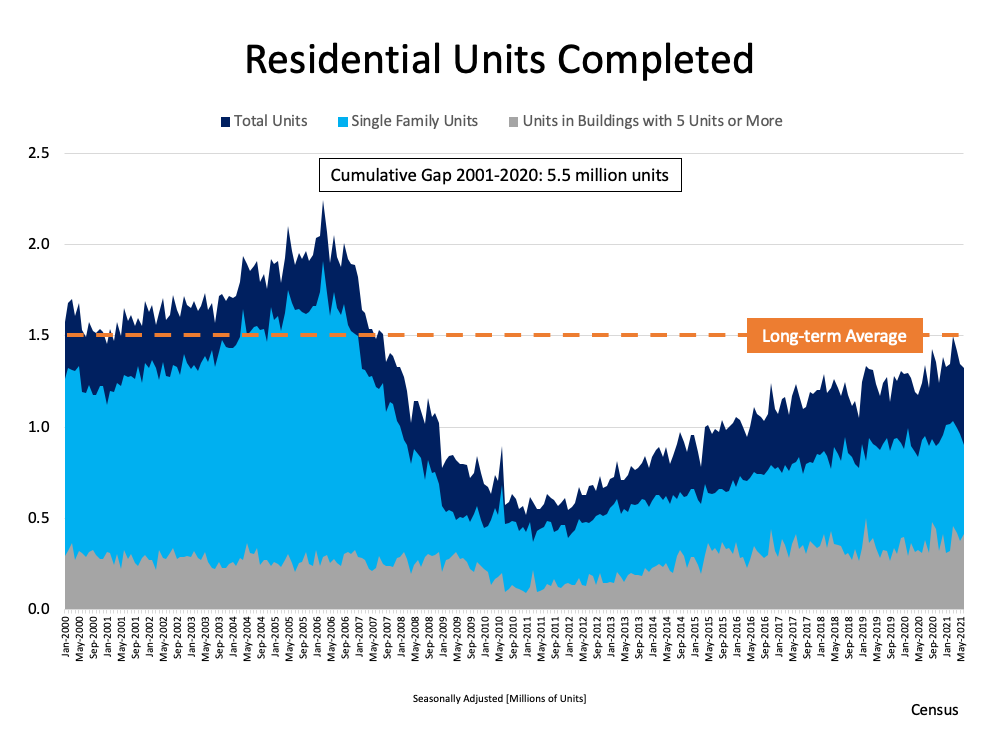

Ever since the housing bubble in 2008, the level of new home construction has been below average.

Dr. Steve Sjuggerud, of Stansberry Research, states just how imbalanced our current supply and demand is,

“Building over the last 20 years was down 5.5 million housing units. And that’s during a time when the U.S. population grew by nearly 50 million people.”

He goes on to explain that in the unlikely scenario that building doubled from the 20-year average, it would still take six years to make up for the shortfall in housing.

WHERE ARE HOME PRICES HEADED?

That low supply and strong demand from the upcoming millennial generation that is reaching homebuying age in large numbers will likely fuel price increases from now until 2022.

Experts from three housing industry entities share their predictions for how much home prices will appreciate from now until next year:

- Fannie Mae: 5.1%

- Freddie Mac: 5.3%

- Mortgage Bankers Association: 8.4%

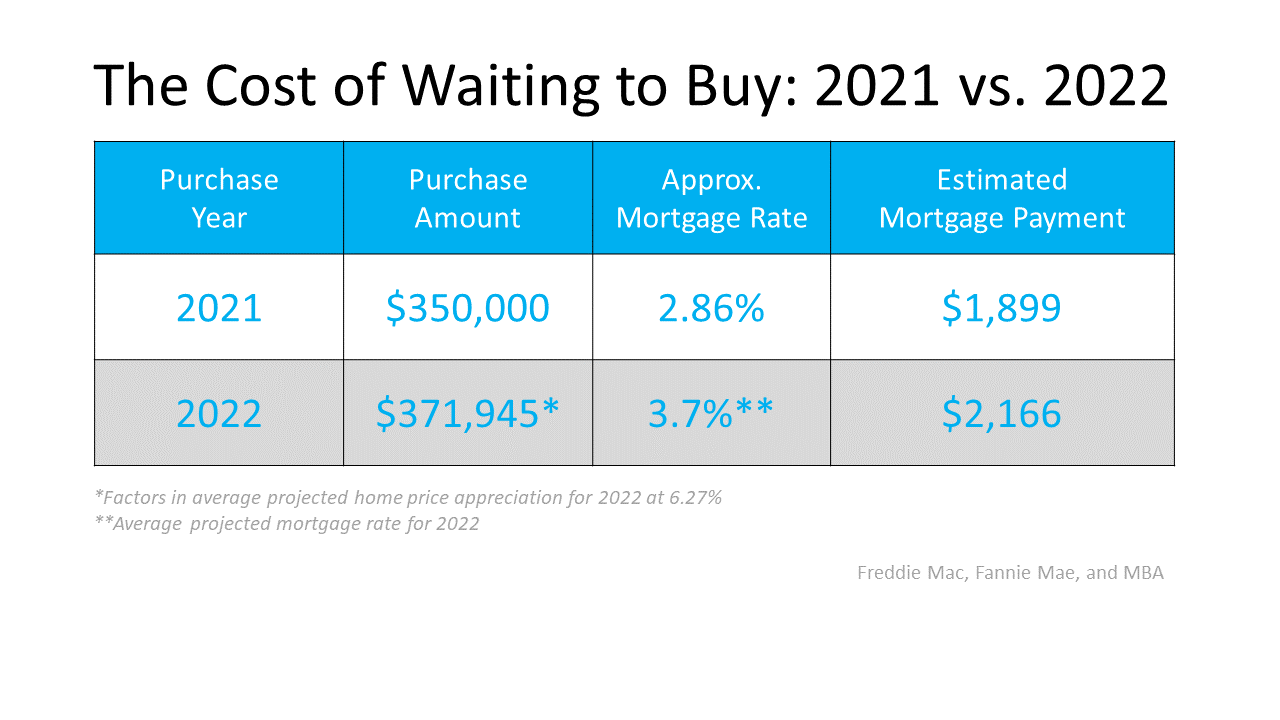

If you average those three estimates (6.27%) and place it on a home worth $350,000 today, its value next year would be $371,945. That’s an extra $21,945 you’re paying for waiting.

WILL RATES RISE?

Our current mortgage rates are some of the lowest we’ve ever seen. This is great news if you can secure a deal today, but what happens if you keep waiting?

The same industry experts from above also shared where they expect mortgage rates to be in 2022:

- Fannie Mae: 3.2%

- Freddie Mac: 3.8%

- Mortgage Bankers Association: 4.2%

We can use their predictions to estimate what a $350,000 home purchase today could look like one year from now.

The chart below shows your potential payments if you keep waiting:

That’s a difference of $267 per month, $3,204 more per year, and a total of $96,120 over the entire loan!

You should also note that the house bought this year would gain about $22,000 in equity and an increase of $118,000 in net worth for the owner.

BOTTOM LINE

Waiting could end up being a very expensive decision. If done correctly, it could build massive wealth for you and your family!

Are you ready to make a move? Fill out the form below and schedule a consultation with one of our mortgage advisors. We will look at all aspects of your financial situation and present you with mortgage options that will maximize your wealth and help you take advantage of the opportunity that is out there today.